27 June 2022

Weekly Market Review (27 June 2022) - What happened and What's Next

Market update

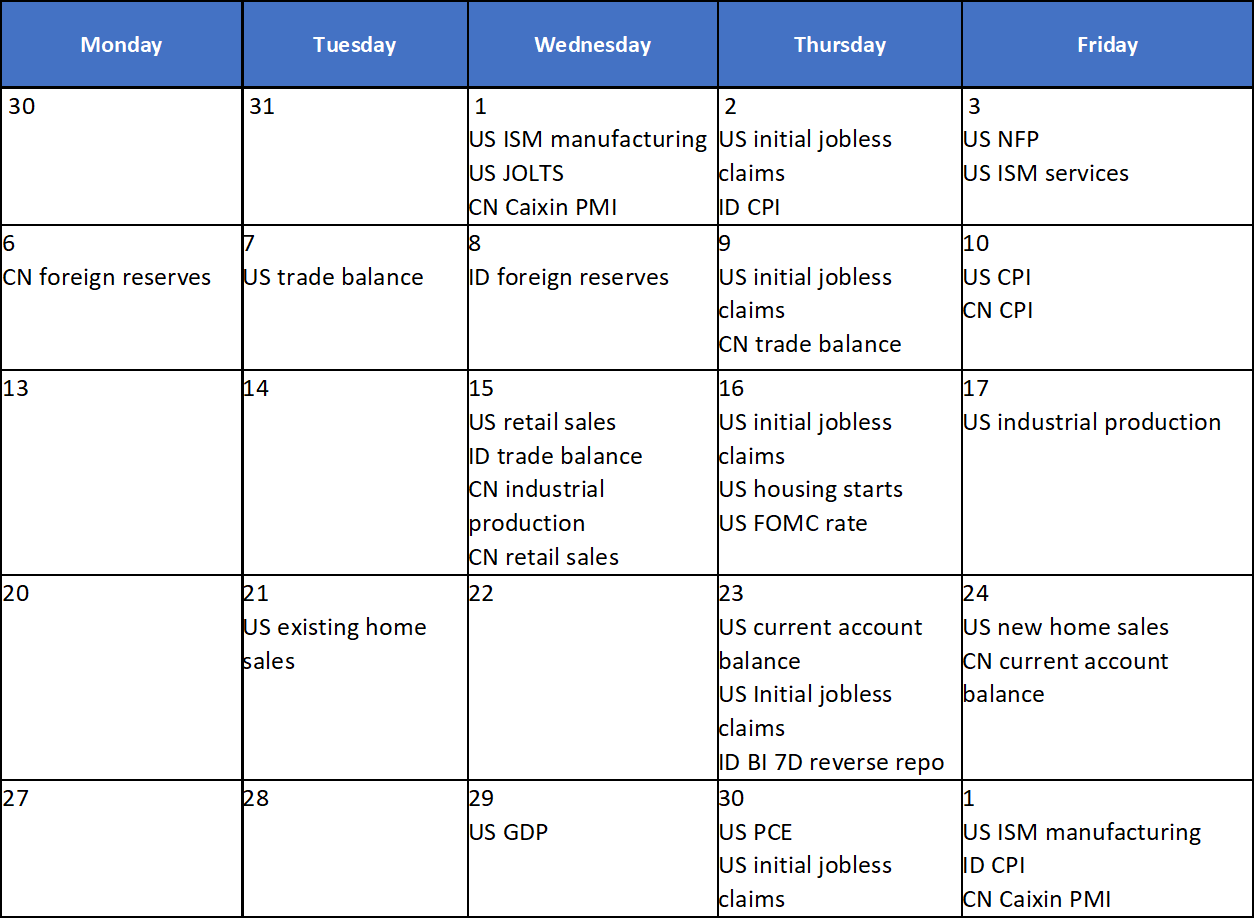

- Global indexes closed higher last Friday ending the three consecutive weeks of losses with S&P 500 and Dow Jones up by +6.4% and +5.4% WoW, respectively. Fed Chairman Jerome Powell highlighted that a soft landing had become “very challenging,” suggesting that getting inflation under control could lead to a recession, suggesting that it might mean less-aggressive rate increases in the future. Expectations for inflation in the University of Michigan consumer sentiment survey also dipped from the preliminary read earlier this month. Now, the odds of the federal-funds rate hitting a range of at least 3.25% to 3.5% in November fell to 50%, down from 71% a week ago. On the domestic side, JCI also booked a gain of +1.5% WoW. Outperformance came from Consumer sector, up by +5.7%% WoW. Meanwhile, Transportation sector led the underperformance, down by -3.6% WoW. News flows to be watched within this week: US PCE, ISM manufacturing, initial jobless claims; China PMI; Indonesia CPI.

- Rupiah weakened by 0.2% WoW to IDR 14,848, in-line with EM currencies. In contrast, DXY weakened by -0.5% WoW to 104.2.

- INDOGB mainly strengthened this week, tracking UST movement with the UST 10Y yield tumbling back towards 3% amid recession fears. Bonds in the 7-20Y area outperformed today with yields down in range of 9-14bps. By the end of the week, 10yr INDOGB was reported at 7.27%.

- Total incoming bids on Tuesday conventional bond auction lowered from the previous auction, reaching IDR 35.1tn. The biggest demand still came for 10yr which reported at IDR 17.8tn. The government rejected all incoming bids for the 15yr and 29yr. Government finally issued IDR 18.9tn or lower than IDR 20tn initial target.

- Based on DMO data, foreign ownership as of 22nd June was reported at IDR 786.70tn or 16.32%

- Treasury yields fell as Powell reiterated a commitment to reining inflation and falling economic prices underline economic growth fears. Bond market volatility remains intense with inflation and recession fears lingered. By the end of last week, 10yr UST was reported at 3.13% (-12bps WoW).

Global news

- US existing home sales in May 2022 recorded -3.4% MoM, in-line with consensus estimate of -3.7% MoM.

- US new home sales in May 2022 recorded +10.7% MoM, higher than consensus estimate of -0.2% MoM.

- US initial jobless claims recorded 229k, in-line with consensus estimate of 226k.

Domestic News

- •Bank Indonesia maintains benchmark rate (7DRR) at 3.5% for 17 consecutive months. USDIDR continues to be stable at 14,800-14,900 range. Meanwhile, Bank Indonesia decision to increase reserve requirement is expected to reduce excess liquidity by IDR 350tn.

- May 2022 banks sector data: loans growth 9.0% YoY/deposit growth 9.9% YoY/TD rate decline to 2.86% or -75bps YoY.

- Bank Indonesia estimates June CPI at 0.5% MoM in weekly survey. Higher prices of food commodities such as chili, shallot, egg, as well as airfare are among the primary inflation drivers for the month.

- The gov't decided to cancel the implementation of the carbon tax policy, from the implementation plan starting July 1, 2022. This is the second cancellation of the April 1 2022 plan as mandated by the HPP Law.

- Govt recorded state budget surplus of IDR 132.2tn (0.74% of GDP) in May 22. State revenue is booked at IDR 1,070.4tn (+47.3% YoY, 58% of target) State expenditure reached IDR 938tn (-0.8% YoY, 34.5% of target).

- Ministry of Finance expects that economic growth in 2Q22 may reach 4.8% - 5.3% YoY.

Calendar

June

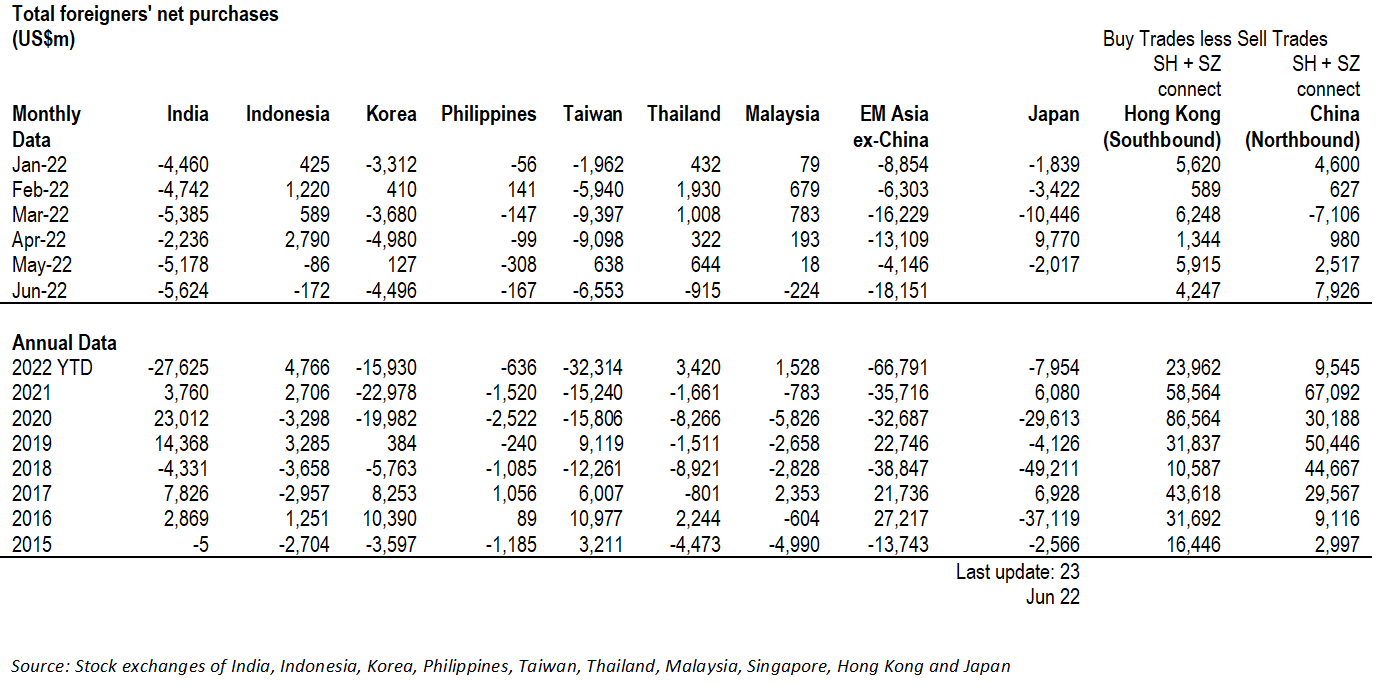

EM Equities Net Foreign Flow