04 July 2022

Weekly Market Review (04 July 2022) - What happened and What's Next

Market update

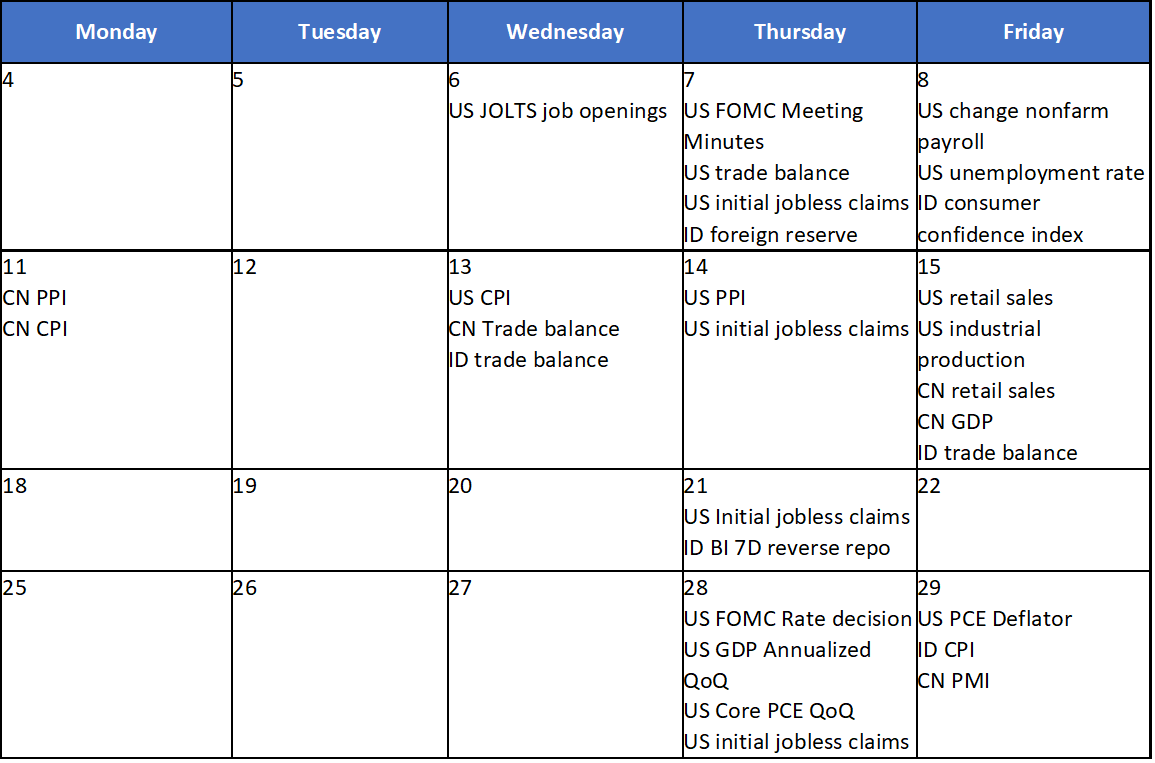

- Global indexes were in the red zone as recession fear led risk assets (stocks, commodities) declined, but ‘safe-haven’ assets such as treasuries gained this past week. US Index edged lower after the last week rebound with S&P 500 and Dow Jones down by -2.2% and -1.3%WoW, respectively. First half of 2022 was tumultuous ride, whereby in the early year we saw index recorded all-time high but then closed out as the worst-first half performance in a decade. Markets remain torn between the implications of clearly slowing US growth but still-high inflation that keeps the Fed erring on the more hawkish side. US May consumption data and revisions to Q1 GDP suggest a softer backdrop for consumer spending, while weaker details of ISM manufacturing reaffirm slowing goods demand. MSCI Asia ex Japan also booked a loss, down by -1.7%WoW. However, although developed world recession, it does not mean a recession in Asia, meaning Asian earnings can still post growth, opening future opportunity. In line with the region, domestic side, JCI dropped by -3.5%WoW. All sectors mostly were in the negative territory, except Healthcare sector which gain by +1.1%WoW. The worst performer was shown by Basic Materials sector, down by -8.1%WoW. News flows to be watched within this week: US change in non-farm payroll, unemployment rate, JOLTS job opening, FOMC meeting minutes, initial jobless; Indonesia foreign reserve, consumer confidence index.

- Rupiah continued to weaken by 0.6% WoW to IDR 14,938, in-line with EM currencies. In contrast, DXY strengthened by 0.9% WoW to 105.1.

- INDOGB yield rallied across the curve rallied by 10bps tracking lower UST. Finance minister recently announced that it cuts target gross issuance for 2022 by IDR216tn to IDR1,084tn from previous IDR1,300tn. By the end of the week, 10yr was reported at 7.25%. (-2bps WoW)

- Total incoming bids in Sukuk auction increased slightly from the previous auction reaching IDR 15.8tn. The short and long tenors attracted higher demand as the 2yr and 11.7yr had incoming bids of IDR 5.4tn and 4.8tn or reaching 34.3% and 30.3% of the total incoming bids respectively. The government also rejected all bid for 6mo- SPNS. The government issued IDR7.8tn.

- Based on DMO data, foreign ownership as of 30th June was reported at IDR780.22tn or 16.09%

- US Treasury yields fell as recession fears and disappointing economic data left market looking to safety assets. Stubbornly high inflation levels and the Federal Reserve’s efforts to tackle a surge in prices have resulted in escalating recession worries. By the end of last week, 10yr UST was reported at 2.98% (-5bps WoW).

Global news

- The US Core Personal Consumption Expenditure (Core PCE) deflator slowed in the third straight month from February’s high of +5.3% YoY to +4.7%YoY in May, suggesting a weaker economy amid the continued inflation and the rate hike cycle. This figure seems on track to meet the Fed’s forecast of 4.3% for 4Q22. However, the headline PCE deflator which was +6.3%YoY (unchanged), made little progress towards the Fed’s 5.2% target.

- US weekly jobless claims edged lower to 231k from revised 233k the week before (but higher than consensus estimation of 230k). The figure stands just above the 2019 pre-pandemic weekly average of 218k when labor market was also strong.

- US Manufacturing PMI posted down in June on the back of contraction in client demand. According to the S&P, Manufacturing sector PMI down to 52.7 in June (lower than prior figure of 57 but slightly better than consensus estimation of 52.4). Output seen broadly flat as firms see a fresh drop in new orders.

- China Caixin Purchasing Manager Index (PMI) which an independent snapshot of the country’s manufacturing sector rose to 51.7 from 48.1 in the prior month and higher than consensus estimation of 50.2. As above 50 means expansionary, the manufacturing activity indicated rebound from prior contraction as covid curbs eased.

Domestic News

- Indonesia Headline Consumer Price Index (CPI) in June grew by +4.35%YoY, higher than consensus estimation at +4.19%YoY and +3.55%YoY in May. This was driven from volatile food such as chili and red onion amidst surging global food prices and La Nina impact. Meanwhile, core inflation steadily picked up by +2.63%YoY (vs +2.58%YoY in May), but this was below consensus of 2.7%YoY.

- Indonesia’s manufacturing PMI decreased to 50.2 in June (from 50.8 in May). The manufacturing production improved on the back of the expansion in order book volumes, in which companies have started stock building to meet the increasing demand.

- The government has reduced the budget deficit target in the 2023 RAPBN to the range of 2.61-2.85% of GDP. The upper limit of the deficit level is lower than the previous government's proposal of 2.9% of GDP, which is contained in the Macroeconomic Framework and Fundamentals of Fiscal Policy (KEM PPKF) 2023.

- Fitch Ratings has affirmed Indonesia's Long-Term Foreign-Currency Issuer Default Rating at 'BBB' (investment grade) with a Stable Outlook. According to Fitch, key factors that support the affirmation are Indonesia's favourable medium-term growth outlook and a low government debt/GDP ratio. However, Fitch underscores several challenges, including higher external debt ratios, low government revenues, and weak structural features.

Calendar

July 2022

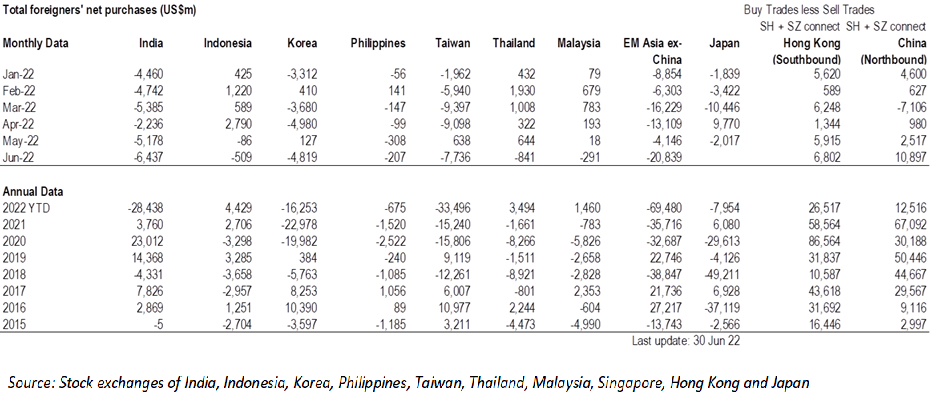

EM Equities Net Foreign Flow