03 October 2022

Weekly Market Review (03 Oct 2022) - What happened and What's Next

Market update

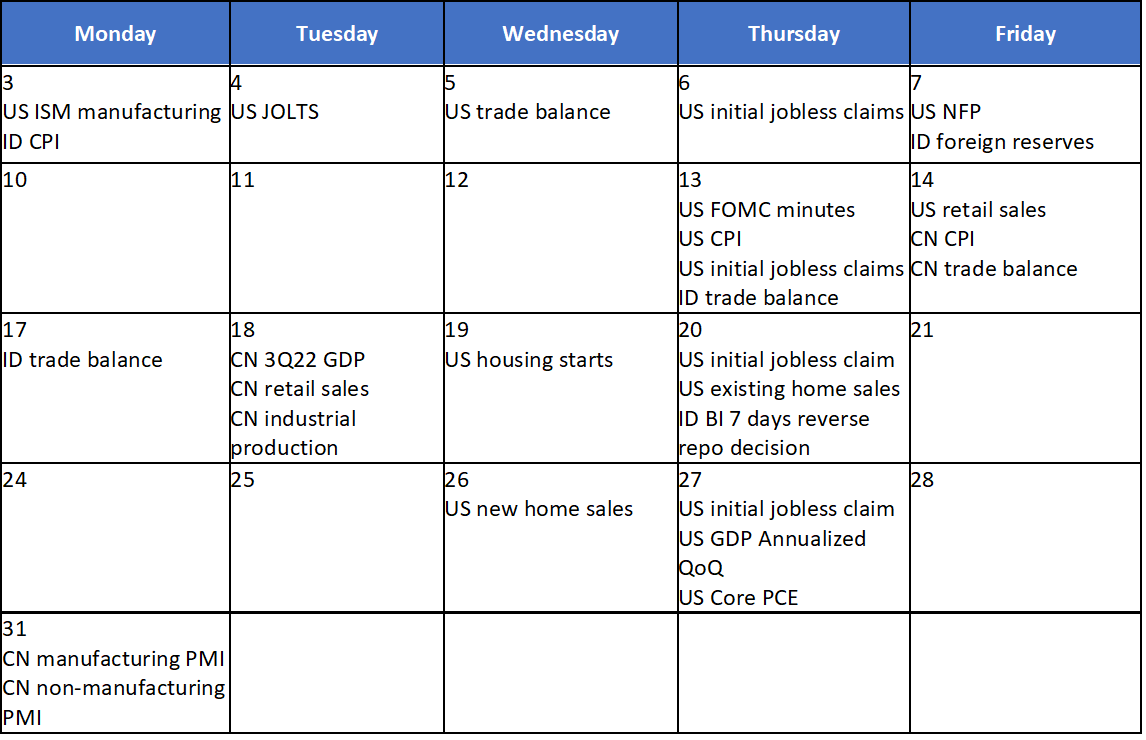

- Global indexes continued its decline last week with DJI and SPX each down by -2.9% WoW. News on Bank of England's (BOE) intervention in the bond market caused worries on financial markets and sent equities lower on Wednesday. BOE bought long-dated bonds and will suspend its plan to gilt selling to try stabilizing the bond market. In addition, several US economic data released last week showed continue resilience in the inflationary pressure despite tightening monetary policy. Weekly jobless claims fell to 193k, well below consensus expectations, and reached its lowest level since late April. Meanwhile, the core PCE index (excludes food and energy) jumped to 4.9% YoY in Aug-22 from 4.7% in the previous month. Similarly, JCI also booked a loss of -1.9% WoW. The main underperformer was industrial sector, down -6.2% WoW. On the other hand, financial sector was most resilient, only declined by -1.3% WoW. News flow to be watched within this week: US ISM manufacturing, US JOLTS, US trade balance, US initial jobless claims, US NFP and ID foreign reserves.

- Rupiah continued to depreciate by -1.3% WoW to IDR 15,228, one of the worst performing currencies in EM. DXY also weakened by -0.9% WoW to 112,12.

- INDOGB traded lower for the week following higher UST and DXY. 5yr INDOGB yields dropped by 24bps over the week to 6.61%. Meanwhile the 10yr INDOGB rose by 12bps to 7.23%.

- Incoming bid on Tuesday conventional bond auction slowed following higher UST and DXY, reaching only IDR 23.7tn compared to previous auction of IDR 52.1tn. Compared to the previous bond auction, all series’ bids dropped, while the upcoming 10yr benchmark still attracted the biggest demand reaching IDR 10.9tn or 45.9% of total incoming bids. The government issued IDR 10.7tn, lower than initial target of IDR 19tn.

- The government did private placement as a part of BI burden sharing program totaling IDR 16.6tn for sukuk for VR series.

- Based on DMO data, foreign ownership as of 26th Sep was reported at IDR 740.68tn or 14.65%.

- 10yr treasury yields rose as high as 4% before eased back to 3.83% (+14bps WoW) as markets jitters about Fed economic policy and series of hawkish comments from Fed. The central bank has made clear that fighting persistent inflation is top of their agenda. Market concerns about interest rates rising too quickly and leading to a recession are rising. Meanwhile yield inversion continued with 2yr UST reported at 4.22% (+2bps WoW).

Global news

- US new home sales was at 685k in Aug-22, well above consensus expectation of 500k and prior month's figure of 532k.

- US initial jobless claims last for a week ended 24 Sep-22 only recorded 193k addition, much lower than expectation of 215k and previous week's at 209k.

- US core PCE index was up by +4.9% YoY in Aug-22 vs consensus expectation of 4.7% YoY and higher than +4.6% figure in Jul-22.

Domestic News

- 2022 State Revenue and Expenditure Budget (APBN) prints a surplus of IDR 107.4tn or 0.58% GDP as of Aug-22.

- The Minister of Finance stated that the realization of BBM direct cash assistance (BLT) reached IDR 6.2 trillion as of 16 Sep-22 or 50% of total budget.

- Indonesia's CPI rose 1.17% MoM in Sep-22, in-line with expectation.

Calendar

October 2022

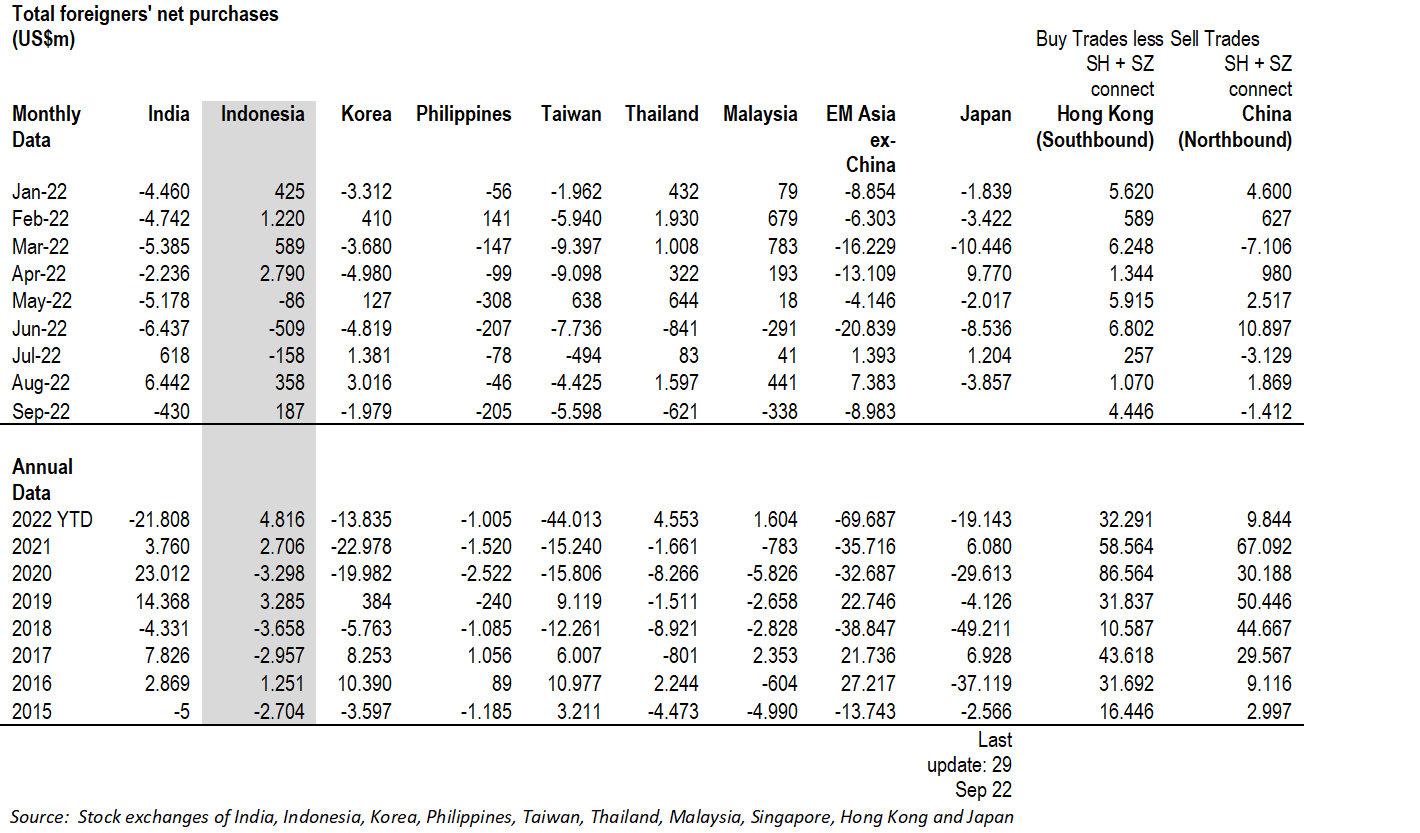

EM Equities Net Foreign Flow